Fintech Loyalty Program Strategy: How Payment Apps Turn Merchant Discovery Into Loyalty

Updated on:

Traditional loyalty programs usually start with a merchant and work outward.

You shop at one retailer. You earn points. You redeem at that same retailer or within a limited partner network. The reward model is built around brand preference.

Payment apps and BNPL platforms often reverse that flow.

They start with the payment relationship, then use merchant discovery, embedded offers, cashback, app behavior, and checkout convenience to create repeat engagement across many merchants. The customer does not return only because they love one brand. They return because the app becomes a useful place to browse, save, pay, track, and redeem.

That is what makes the model strategically interesting for loyalty teams.

Merchant discovery is not just a top-of-funnel acquisition tactic in these apps. It becomes part of the loyalty engine. The app shows relevant merchants, gives the customer a reason to shop there, routes the payment through the app's preferred checkout or card rails, and turns that activity into another reason to come back.

The result is a different kind of retention loop: not "earn points at my store," but "keep shopping through my ecosystem because that is where the value compounds."

Key findings

Payment apps often use merchant discovery as a loyalty engine: users browse offers, shop through the app, pay with the app's rails, and come back because the value sits inside the ecosystem.

In these models, convenience can be the reward. Fast checkout, saved identity, flexible payment options, and in-app offer visibility can matter as much as points.

Merchant-funded offers and cashback help wallet apps scale rewards without carrying the full cost of every incentive themselves.

Revolut, PayPal, Klarna, Affirm, and Cash App/Afterpay all use different versions of the same loop: attract attention with utility, deepen engagement with shopping value, and keep the customer inside the payment relationship.

The best lesson for loyalty teams is not "copy fintech." It is "design reward loops around the surfaces customers already use most."

In BNPL and credit-adjacent products, loyalty design needs tighter guardrails because pushing repeat usage without regard to repayment behavior or risk can create trust and regulatory problems.

What does "merchant discovery into loyalty" actually mean?

In a fintech or payment-app context, merchant discovery becomes loyalty when four things work together:

The app helps the user find merchants, offers, or categories worth exploring.

The app makes payment or financing easier than doing it elsewhere.

The app gives the user a reward, savings benefit, or convenience benefit for staying inside the flow.

The reward or utility is visible enough that the customer has a reason to come back next time.

That reward does not have to be a classic points balance.

It can be:

cashback

merchant offers

app-exclusive 0% financing

faster checkout

one-click identity and saved payment

partner-funded rewards

card-linked acceleration

travel-style redemption

balance growth inside the app

The key is that merchant discovery is no longer a one-time browse feature. It becomes part of the retention architecture.

Why this model is growing

Wallet and BNPL apps have a structural advantage here: they sit close to payment intent.

A retailer has to convince a customer to sign up for a brand-specific rewards program. A payment app is already trying to be present at checkout, in the shopping journey, or in the user's financial routine. That means it can attach loyalty mechanics to behavior the customer already performs:

browsing merchants in-app

choosing a pay-later option

checking out with a saved identity

activating an offer

using a wallet balance or linked card

managing a payment plan

returning to see what else is available

For the operator, that changes the economics. Instead of funding every reward directly, the app can use merchant-funded offers, interchange-related logic, partner commissions, financing revenue, subscription-plan benefits, or ecosystem expansion to support the loyalty layer.

Example 1: Revolut uses merchant discovery to deepen wallet behavior

Revolut's RevPoints program is one of the clearest examples of a fintech app turning product discovery into loyalty.

Based on Revolut's official RevPoints pages and help documentation, users can earn points not only from eligible card spending, but also through Stays, Experiences, Shops, spare-change conversion, and Revolut Pay. In its Shops flow, Revolut lets users browse participating brands, activate offers, and earn extra RevPoints when they shop through those merchant paths.

That matters because Revolut is not rewarding only card usage. It is rewarding ecosystem usage.

The loyalty loop looks like this:

hold a Revolut account

spend on card or via Revolut Pay

browse Shops, Stays, or Experiences

earn RevPoints at different rates depending on plan and activity

redeem into airline miles, gift cards, stays, experiences, or checkout discounts

The lesson for loyalty managers is useful: merchant discovery becomes stronger when it is connected to a broader value system. In Revolut's case, discovery is not a floating marketplace tab. It is connected to points, paid-plan differentiation, checkout preference, and redemption paths.

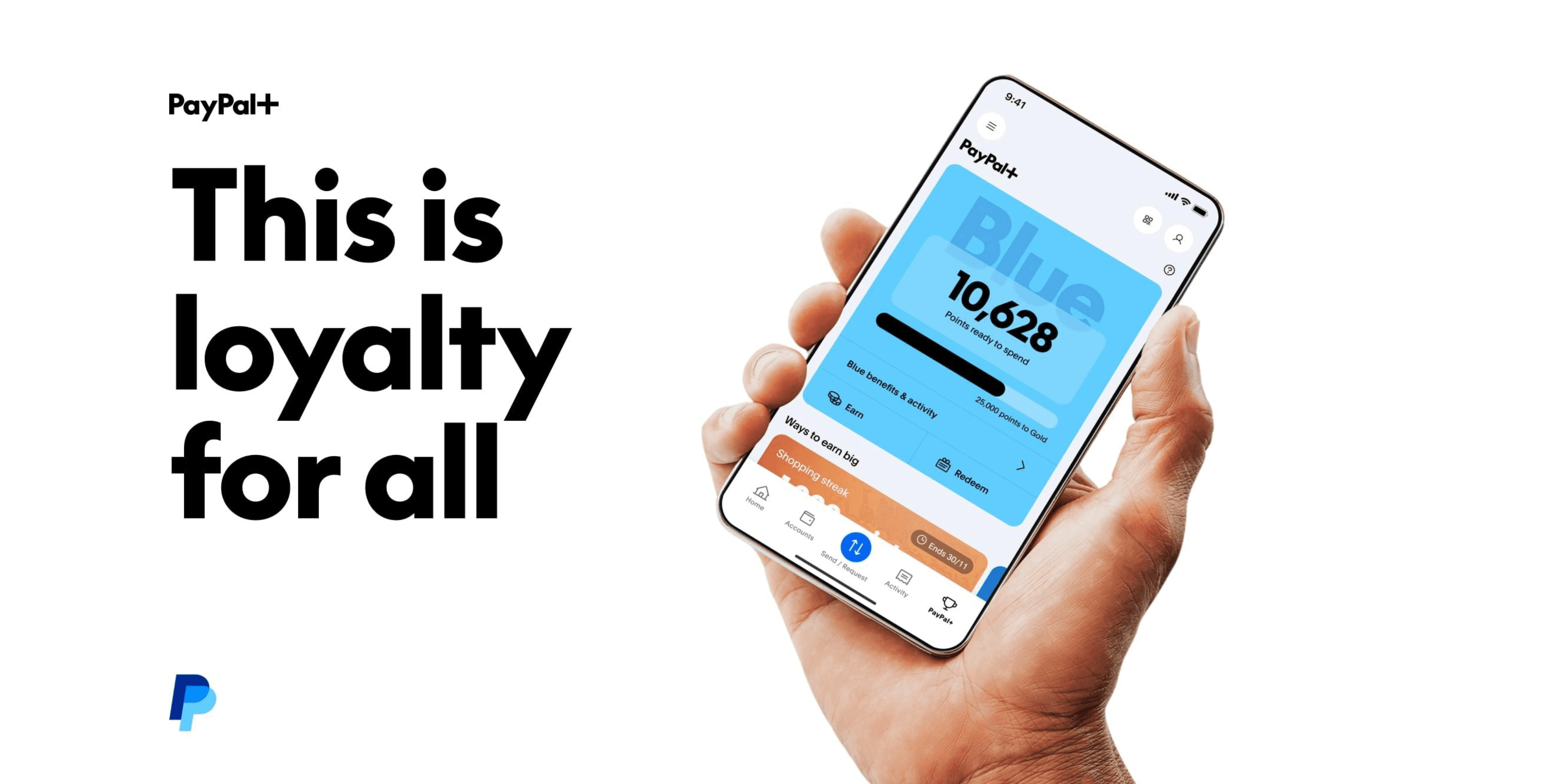

Example 2: PayPal turns checkout identity into a rewards surface

PayPal Rewards shows a slightly different model.

PayPal's official rewards and digital wallet pages position the app as the place to find offers, check out with PayPal, track rewards, and redeem them. The customer does not need to join a separate merchant club for each brand in the network. Instead, PayPal uses wallet identity and checkout routing as the loyalty layer.

The loop here is:

open the app

see offers from participating brands

check out with PayPal

earn rewards or stack them with linked PayPal card benefits

redeem into PayPal balance, savings, donations, or future purchases

This is merchant discovery turning into loyalty in a very specific way: the customer learns that using PayPal is not just a payment option. It is also the path to a better shopping outcome.

That is an important distinction. The loyalty object is not only the merchant. It is also the payment behavior.

For CXForge readers, the takeaway is that offers feel more loyalty-like when the customer can see, track, and redeem value in one place. Fragmented rewards do not create much retention. Visible, reusable value does.

Example 3: Klarna blends shopping discovery, cashback, and payment flexibility

Klarna's app brings the model even closer to a commerce ecosystem.

Its official app and cashback pages highlight a mix of:

cashback on participating merchants

flexible payment options

Klarna balance

price comparison

loyalty-card storage

online and in-store shopping

Klarna is not relying on a simple "buy now, earn points" setup. It is creating a shopping environment where users browse merchants, discover deals, choose how to pay, earn cashback, and keep that value inside the Klarna balance or broader app relationship.

One especially useful detail from Klarna's own materials is that Klarna frames cashback as separate from a merchant's own loyalty program. In practice, that means the user can often earn Klarna cashback and still earn a retailer's regular loyalty points.

That is powerful because it lowers resistance. The app is not asking the user to abandon existing brand loyalty. It is adding another layer of value on top.

For loyalty teams, this is a strong lesson: if your reward model complements existing customer behavior rather than trying to replace it, adoption gets easier.

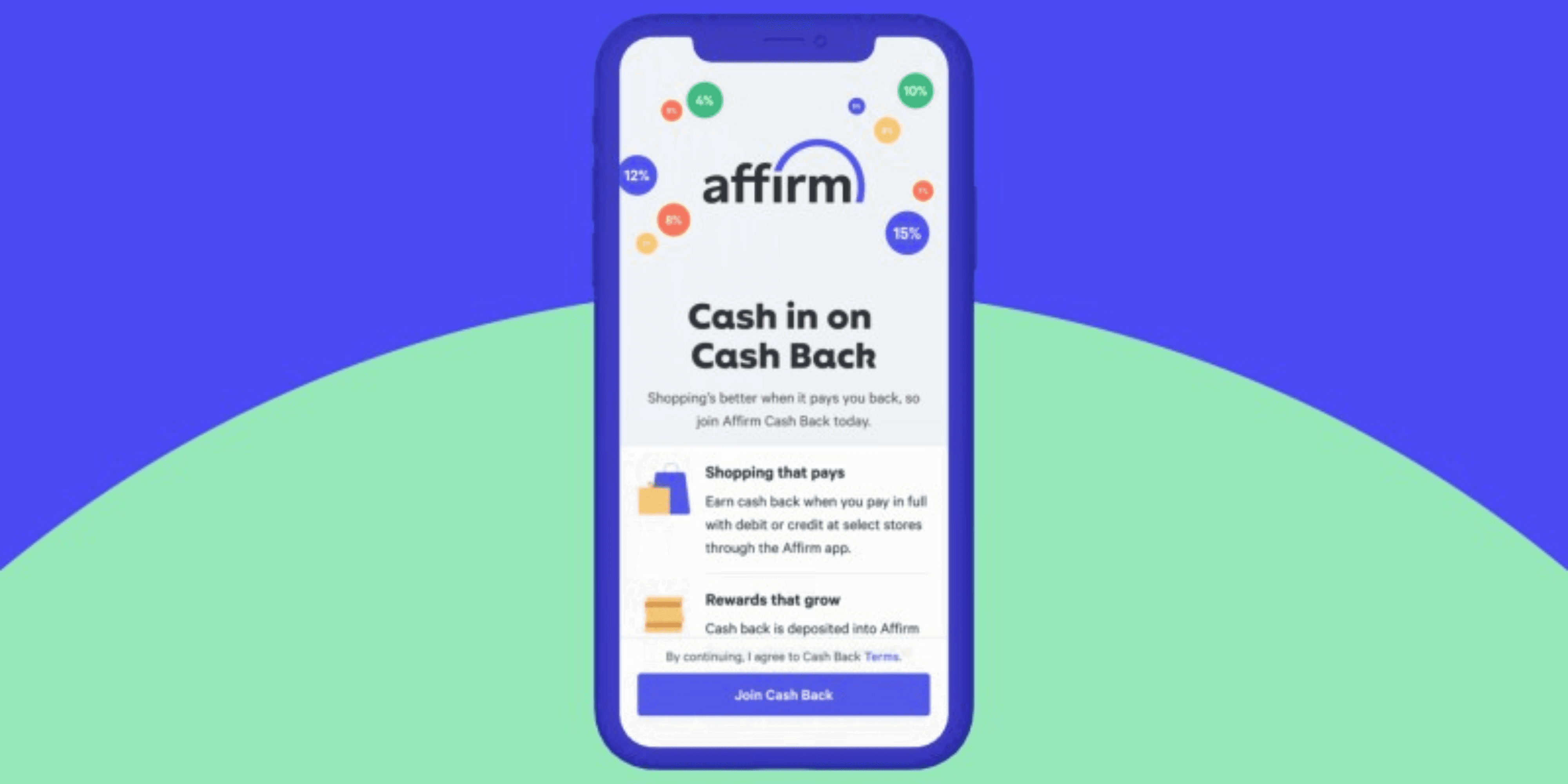

Example 4: Affirm uses offer access more than classic rewards

Affirm is a useful counterexample because it shows that loyalty does not always need a visible points currency.

In its app-related announcements, Affirm emphasizes:

shopping anywhere

merchant discovery

exclusive 0% or low-APR offers

browser extension and app convenience

prequalified spending confidence

This is still a loyalty model. It just does not look like a traditional rewards club.

The customer returns because the app helps them find financing value and shopping opportunities they may not get elsewhere. In this kind of model, the reward is not "you earned 500 points." The reward is "this app makes it easier and cheaper to buy from merchants I care about."

That can be a powerful loyalty loop, but it also carries a different responsibility. If the operator overuses financing incentives without enough transparency or repayment sensitivity, the retention model can drift into dependency instead of healthy loyalty.

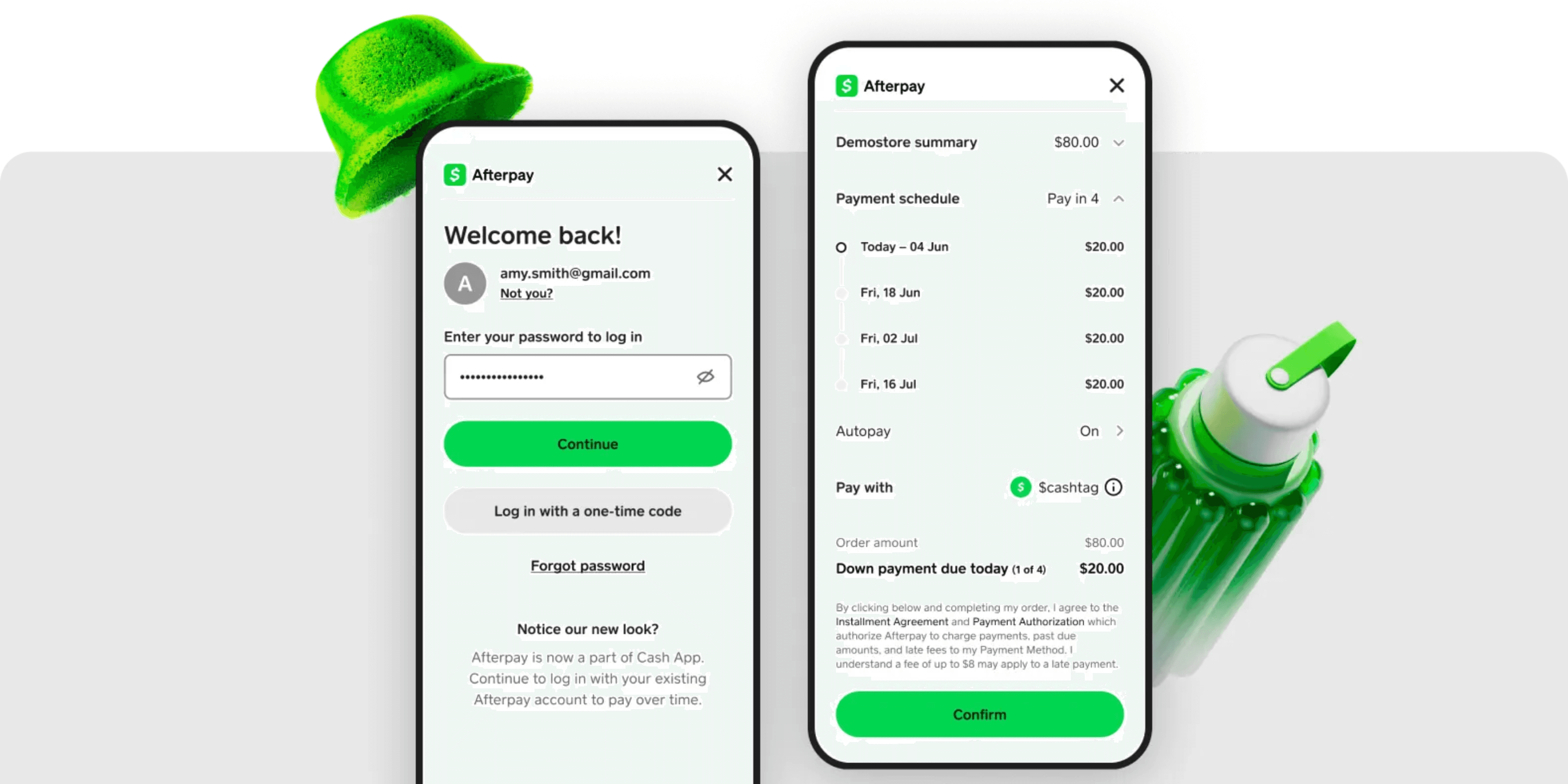

Example 5: Cash App and Afterpay show the wallet-BNPL convergence

Cash App's Afterpay integration shows another version of the same pattern.

Rather than leaving BNPL as a detached checkout feature, Cash App pulls Afterpay into the broader wallet relationship. Users can pay over time, manage purchases inside Cash App, and in some cases extend eligible past card purchases into installment repayment.

This matters because the app becomes more central to the user's financial behavior:

spend with the card

manage money in the wallet

use pay-over-time when needed

return to the app to monitor purchases and payments

That is not classic merchant discovery in the marketplace sense, but it still creates a loyalty effect. The more financial jobs the app does well, the more likely the user is to keep it in the center of future purchase decisions.

What loyalty teams should learn from these models

The point is not that every retailer should become a fintech app.

The point is that these apps are good at building retention around the behaviors customers repeat most. Loyalty managers can borrow that mindset.

1. Put rewards close to the customer's decision path

The strongest fintech-style loops do not hide rewards in a monthly email. They put value where the customer is already deciding:

merchant list

checkout flow

saved payment method

in-app balance

financing choice

post-purchase management

2. Treat discovery as part of retention, not only acquisition

If a customer keeps returning to your environment to see what is available, your discovery surface is already part of the loyalty product.

That could mean:

partner offers

category curation

local recommendations

cross-merchant bundles

3. Make redemption immediate or obviously useful

Visible value matters.

Revolut does this through travel-style redemptions and checkout discounts. PayPal does it through reward tracking and wallet redemption. Klarna does it through cashback balance. The pattern is the same: the customer needs to feel the value is real and reachable.

4. Let partners help fund the reward layer

Merchant-funded offers are attractive because they can scale better than self-funded discounting. But they need careful governance. If the offers are too inconsistent, too broad, or too hard to understand, they stop feeling like loyalty and start feeling like coupon clutter.

5. In BNPL or credit-like products, do not reward bad behavior

This is the biggest watchout.

The CFPB's 2025 BNPL research found that many users had multiple simultaneous pay-in-four loans and that one-third borrowed from multiple providers. That does not mean BNPL loyalty is inherently bad. It means the design should be more careful than a standard retail punch-card program.

A responsible BNPL-adjacent loyalty strategy should reward behaviors like:

successful repayment

active account management

offer relevance

healthy repeat engagement

merchant discovery quality

It should be much more cautious about rewarding raw borrowing frequency alone.

A practical framework for building this kind of loyalty

If you are designing a wallet, payment app, or BNPL-adjacent rewards system, the framework is simpler than it looks.

Step 1: Decide what behavior you actually want

Do you want:

more monthly active users?

more checkout share?

more offer activation?

more in-app merchant discovery?

more plan upgrades?

more healthy repeat use from good-standing customers?

Pick the behavior first. Then pick the reward.

Step 2: Match the reward to the surface

Different surfaces support different reward types:

Surface | Best-fit reward |

|---|---|

Merchant discovery feed | featured offers, cashback, points multipliers |

Checkout | instant discount, pay-with-points, partner offer |

Wallet balance | cashback, stored credit, savings-linked value |

Financing flow | transparent promotional APR offers, selected merchant benefits |

Subscription or paid plan | accelerated earn rate, exclusive redemption, premium partner benefits |

Step 3: Keep the reward logic understandable

Fintech apps can become confusing fast when they mix:

points

cashback

financing offers

paid-plan multipliers

partner exclusions

redemption thresholds

If customers cannot explain how value is earned and used, the loop weakens.

Step 4: Measure incrementality, not just activity

More app opens are not enough.

Track:

offer activation rate

conversion from discovery to purchase

repeat active users

redemption rate

share of wallet

revenue per active user

merchant-funded reward utilization

repayment health or delinquency risk where credit is involved

support contacts caused by reward confusion

Common mistakes

The most common failure patterns in this category are:

treating every merchant offer as loyalty

overcomplicating rewards logic

rewarding borrowing volume instead of healthy engagement

hiding redemption rules

letting partner offers feel random or low quality

failing to connect rewards to the customer's main app behavior

chasing growth without measuring trust or repayment health

Final takeaway

Payment apps turn merchant discovery into loyalty by making shopping value part of the payment relationship.

That value may look like cashback, points, checkout discounts, financing offers, card-linked rewards, or ecosystem perks. But under the surface, the principle is the same: the app becomes more valuable each time the customer shops through it, pays through it, or redeems through it.

For loyalty teams outside fintech, that is the useful lesson.

Do not think only in terms of "points after purchase." Think in terms of where the customer discovers value, how easily they can act on it, and whether the reward makes them want to return to the same surface next time.

That is where loyalty starts to feel less like a promotion and more like product design.

FAQ

What does it mean to turn merchant discovery into loyalty?

It means the app does more than list merchants or offers. It uses discovery, payment, and rewards together so the customer has a reason to keep coming back to the same ecosystem for future purchases.

Is merchant-funded cashback the same as a loyalty program?

Not exactly. Cashback and merchant offers can act like a loyalty layer, especially when they are tied to app identity, redemption, and repeat engagement. But by themselves, they are not always a full loyalty program.

What can loyalty managers learn from Revolut, PayPal, and Klarna?

They can learn how to place rewards close to checkout, use merchant-funded value more efficiently, and make redemption visible and practical. They can also learn that discovery and convenience can be loyalty drivers.

Are BNPL rewards programs risky?

They can be if they reward borrowing volume without enough regard for repayment behavior, customer risk, or transparency. In BNPL and credit-adjacent products, responsible design matters more.

Which metrics matter most in this model?

Offer activation, conversion from discovery to purchase, repeat active users, redemption rate, revenue per active user, share of wallet, and repayment health where financing is part of the proposition.

CXForge helps loyalty and retention teams connect customer identity, reward logic, offer orchestration, and cross-channel reporting into one system.

If your team is rethinking how discovery, rewards, checkout, and repeat behavior should work together, CXForge can help you design a loyalty model that fits your economics instead of copying someone else's app surface.